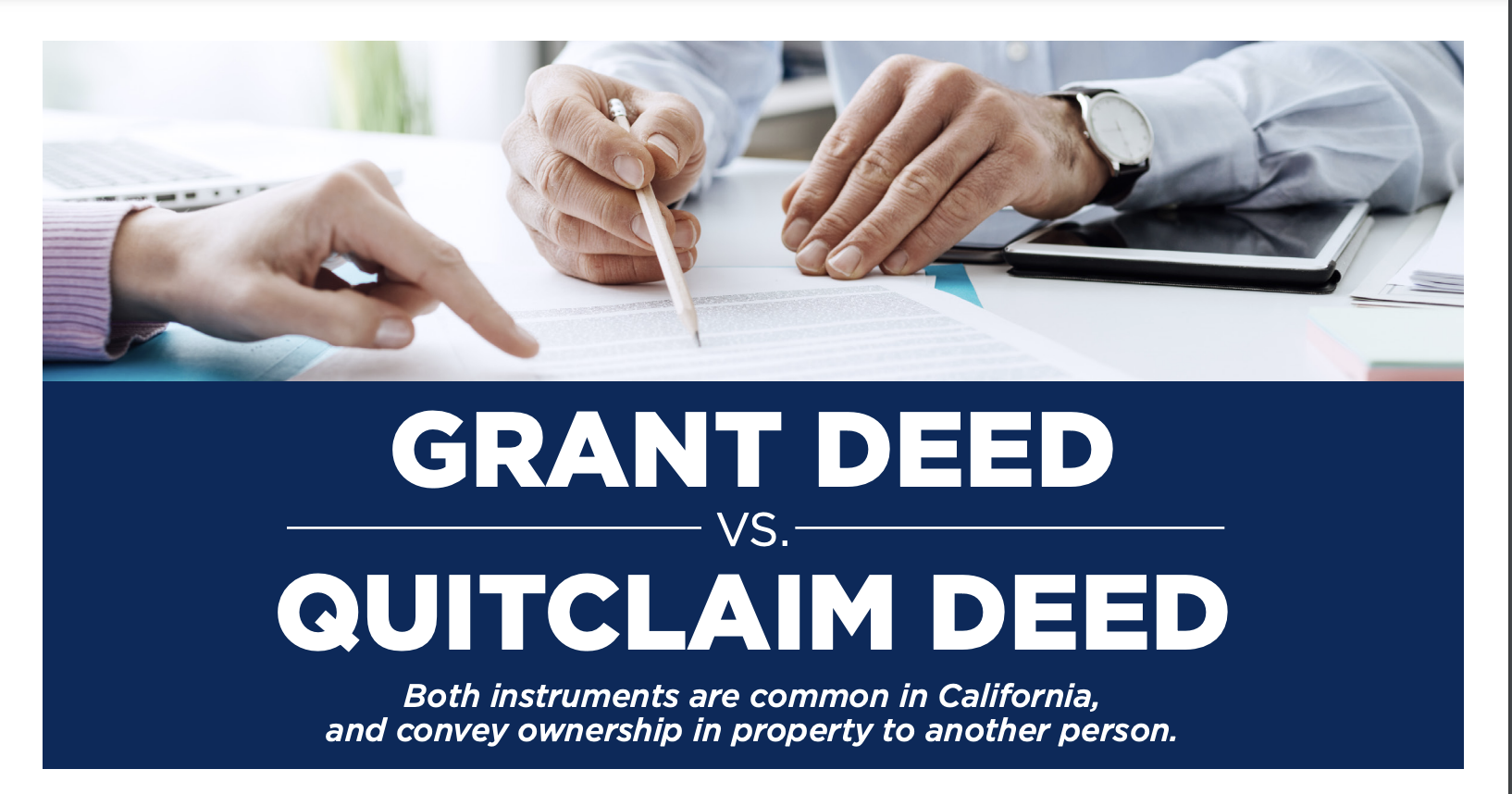

From our friends at Lawyer’s Title, a great infographic on the differences between a Grant Deed and a Quitclaim Deed. This question often comes up, especially in many of our family transactions involving gifts or inheritance or selling below fair market value here in Newport Beach, Costa Mesa or anywhere in the state of California. (other … Continue Reading